Retirement planning often shifts the focus from accumulation to sustainability. For many people, building a durable investment strategy for retirement becomes less about chasing returns and more about aligning growth potential with thoughtful risk management. Market fluctuations, income needs, taxes, and legacy goals all intersect during this stage of life, making coordination essential.

At Barron Financial Group, we believe investment decisions should reflect stewardship, long-term perspective, and family priorities. A well-constructed portfolio is not designed around headlines or short-term trends. Instead, it is built around your time horizon, income structure, and the role your assets play in supporting both present needs and future generations.

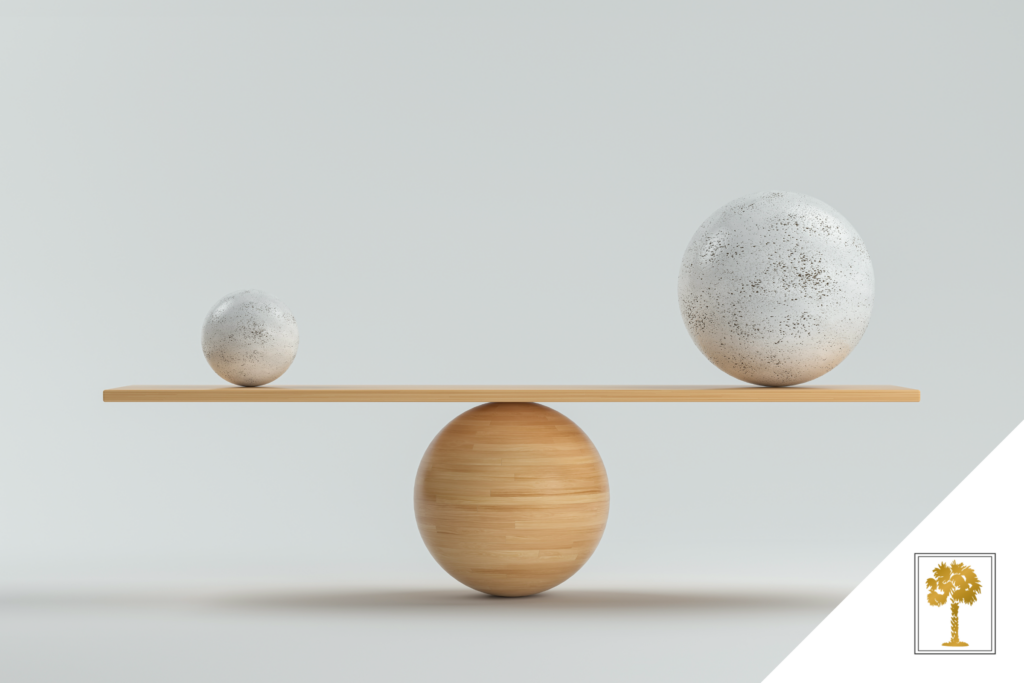

Understanding the Balance Between Growth and Risk

Every investment strategy involves trade-offs. Growth-oriented assets may provide opportunities for appreciation, yet they can also introduce greater short-term volatility. More conservative allocations may reduce fluctuations, though they may not keep pace with inflation over extended periods.

Balancing growth and risk requires clarity around several key questions:

- How much income do you expect your portfolio to provide?

- How long may those assets need to last?

- How comfortable are you with market variability?

- What legacy intentions should be considered?

A durable investment strategy for retirement takes these elements into account rather than focusing on any single metric. The goal is not to eliminate risk, which is not possible in investing. Instead, it is to align risk exposure with your broader financial plan.

The Role of Diversification

Diversification remains one of the foundational principles of long-term investing. By spreading assets across different investment types, sectors, and strategies, a portfolio may respond differently under varying market conditions.

This approach does not prevent losses, and it does not promise specific outcomes. However, diversification can help reduce the impact of concentrated exposure to a single area of the market.

For retirees, diversification also involves thinking beyond asset classes. It may include tax diversification across account types such as traditional IRAs, Roth accounts, and taxable brokerage accounts. Coordinating these elements supports flexibility when income withdrawals begin.

Time Horizon and Retirement Income Planning

One common misconception is that retirement automatically requires a dramatic shift away from growth-oriented investments. In reality, retirement can span decades. A portfolio may need to support income for 20 to 30 years or more.

This longer time horizon often calls for continued exposure to growth assets, balanced by income-producing or more stable components. A durable investment strategy for retirement considers both near-term withdrawal needs and longer-term purchasing power.

Structured retirement income planning plays a central role here. Aligning investment allocations with anticipated withdrawal schedules may help manage how market fluctuations affect income needs. For example, maintaining a portion of assets in more stable vehicles for short-term expenses can allow growth-oriented investments more time to recover during volatile periods.

Risk Tolerance Versus Risk Capacity

Risk tolerance refers to your emotional comfort with market movement. Risk capacity refers to your financial ability to withstand fluctuations without disrupting your goals. Both matter.

Some investors may feel comfortable with volatility but rely heavily on their portfolios for essential income. Others may have substantial reserves yet prefer a steadier allocation.

A durable investment strategy for retirement bridges these two concepts. It aims to align your comfort level with the practical realities of your income plan and legacy objectives. This alignment often evolves over time as life circumstances change.

The Importance of Ongoing Review

Investment strategies should not be static. Tax laws evolve. Market conditions shift. Family priorities change. Healthcare considerations emerge.

Periodic reviews allow adjustments that reflect these changes. This may include rebalancing allocations, revisiting income projections, or evaluating whether your portfolio remains aligned with your stated goals.

At Barron Financial Group, we view investment management as part of a broader planning conversation. Tactical adjustments may be appropriate in certain environments, but they are always evaluated within the context of your long-term financial plan.

Avoiding Emotional Decision-Making

Periods of volatility can create pressure to react quickly. However, frequent, emotion-driven changes may disrupt a carefully constructed strategy.

A clearly defined durable investment strategy for retirement provides a framework for decision-making. When expectations and boundaries are established in advance, it becomes easier to evaluate whether a potential adjustment reflects thoughtful planning or short-term reaction.

This does not mean ignoring new information. It means responding with intention rather than urgency.

Integrating Investments With Legacy Goals

For many families, investment strategy extends beyond personal retirement income. It also intersects with estate considerations and multigenerational wealth planning.

Asset allocation decisions may influence how wealth is transferred, how beneficiaries receive distributions, and how charitable giving strategies are implemented. Coordinating investment planning with estate documents, beneficiary designations, and tax considerations supports a more unified approach.

Building With Purpose

A durable investment strategy for retirement is not about predicting market movements. It is about aligning your portfolio with your values, income needs, and long-term intentions. Growth and caution are not opposing forces. When thoughtfully balanced, they can work together within a comprehensive financial plan.

If you are evaluating whether your current portfolio reflects your retirement goals, income needs, and family priorities, we invite you to connect with Barron Financial Group. Let’s schedule a time to review your durable investment strategy for retirement and discuss how it fits within your broader long-term financial planning.

– Barron-COVER")